The new standard does not provide specific guidance on the presentation of variable lease payments received for direct financing or sales type leases. We believe that presentation as either lease income or interest income may be appropriate, depending on the nature of the lease. In making this determination, Lessors should assess whether the payments are more akin to lease payments or interest.

- Cash flows from the purchase, sale or insurance recoveries of capitalized and noncapitalized collection items are reported as investing actives on the statement of cash flows.

- Noncash investing and financing activities that are unique to not-for-profit entities include contributions of (1) property and equipment, (2) beneficial interest in trusts and (3) marketable securities.

- Similarly, lease liabilities for finance leases are required to be presented separately from lease liabilities from operating leases and from other liabilities.

- Many not-for-profit entities receive donations for which the donor has placed a stipulation that they must be used for long-term purposes, such as the purchase of property and equipment or for endowment funds.

Financial Accounting

For operating leases, the lessee must present both components together as lease expense within income from continuing operations, consistent with the presentation of other operating expenses. Lease expense should be classified within cost of sales; selling, general, and administrative expense; or another expense line item depending on the nature of the lease. In addition to activities that generate cash flows (operating, investing, and financing), companies also engage in investing and financing activities that do not generate any cash flows. Normally, the sale of marketable securities is treated as an investing activity. If however, donated marketable securities are not converted nearly immediately to cash, then the sale of these securities would be reported as an investing activity, whether or not the donation was received with donor-imposed long-term purpose restrictions. Note X. LeasesSusie’s has historically entered into a number of lease arrangements under which we are the lessee.

Hello and welcome to Viewpoint

Assets subject to lease under operating leases should be presented separately from owned assets that are held and used by the lessor as they are subject to different risks. Any rent receivable, deferred rent revenue (i.e., that results from requirement to recognize rents on a straight-line basis), or prepaid initial direct costs would be subject to current and long-term presentation requirements. TransitionThe leasing standard requires an entity to provide the general disclosures required by ASC 250 Accounting Changes and Error Corrections.

Sale of Marketable Securities

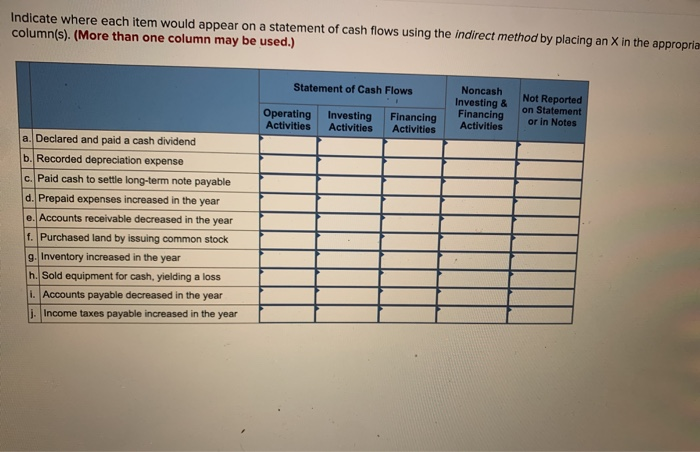

A company does not generate any cash inflows or cash outflows from non-cash investing and financing activities. However, these activities can still have a material effect on a company’s financial position. With that objective in mind, significant judgment will be required to determine the level of disclosures necessary for an entity. From these examples, it is easy current ratio formula to see that non-cash activities can significantly affect a company’s capital composition. As a result, once a significant non-cash transaction is involved, a company must disclose this transaction in its cash flow statement. As shown, there are multiple transactions that require special attention during the preparation of a not-for-profit’s statement of cash flows.

For example, an entity that elects to adopt the new standard as of the effective date (i.e., without restating prior comparative periods), the four prior years in the selected financial data table would not be adjusted. Companies will be required to provide the disclosures required by Instruction 2 to S-K Item 301 regarding comparability of the data presented. Information about all investing and financing activities of an entity during a period that affect recognized assets or liabilities but that do not result in cash receipts or cash payments in the period shall be disclosed. For operating leases, the assets underlying the leases and related depreciation are presented in accordance with other accounting guidance (e.g., ASC 360).

Understanding the correct way to report these transactions on the statement of cash flows can help ensure your organization’s financial position is depicted accurately. As of December 31, 20×9 and 20×8, the weighted-average remaining lease term for all operating leases is 3.4 years and 3.5 years, respectively, while the weighted-average remaining lease term for all finance leases is 4.9 years and 5.6 years, respectively. Upon opening a new retail location, we typically installs brand-specific leasehold improvements with a useful life of eight years. Generally, we do not consider any additional renewal periods to be reasonably certain of being exercised, as comparable locations could generally be identified within the same trade areas for comparable lease rates.

Many not-for-profit entities receive donations for which the donor has placed a stipulation that they must be used for long-term purposes, such as the purchase of property and equipment or for endowment funds. These cash receipts are to be reported as financing activities in the statement of cash flows. Some not-for-profit entities have endowment funds, which have donor-imposed restrictions that restrict the use of the income to long-term purposes.

Cash flows from the purchase, sale or insurance recoveries of capitalized and noncapitalized collection items are reported as investing actives on the statement of cash flows. Non-cash investing and financing activities refer to transactions that affect the company’s investment and financing but do not involve actual cash inflows or outflows during the reporting period. These activities are important for understanding a company’s overall financial health as they can have significant implications for future cash flows, even though they don’t impact the cash flow statement directly. LessorA lessor is required to present lease assets (i.e., net investment in leases) resulting from sales-type and direct financing leases separately from other assets in the balance sheet. Lease assets are financial assets that are subject to current and long-term presentation requirements in a classified balance sheet. If the lessee chooses to report ROU assets and liabilities within other line items on the balance sheet rather than in separate captions, the lessee is prohibited from reporting finance lease ROU assets or finance lease liabilities in the same caption as operating lease ROU assets and operating lease liabilities.

Specifically, of our 250 retail locations, 240 are subject to operating leases and 5 are subject to finance leases. In addition, we lease our corporate headquarters facility, as well as various warehouses and regional offices. We are also a party to an additional 12 leases in which we previously operated a retail location, but which are now subleased to third parties. In addition, we have elected the short-term lease practical expedient related to leases of various equipment used in our retail locations. Lessors must classify all cash receipts from leases as operating activities in the statement of cash flows.

Although ASC 842 removed leveraged lease accounting, leases that met the definition of a leveraged lease under ASC 840 that commenced before the effective date of ASC 842 are grandfathered in. As such, entities that continue to have leveraged leases must continue to provide disclosures as required by ASC , which carries forward existing guidance from ASC 840. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. “Smith & Howard” is the brand name under which Smith & Howard PC and Smith & Howard Advisory LLC provide professional services.