Since updates occur in real-time, businesses can promptly address any inconsistencies that may arise. In contrast, a periodic inventory system only identifies problems during physical inventory counts at specific intervals, making it difficult to pinpoint when an issue occurred and delaying its resolution. The periodic inventory system requires a physical count of inventory at the end of the period. Most companies using periodic inventory systems are small businesses that only count inventory and calculate COGS once per year. However, if you want to use the periodic inventory system monthly, you can estimate the units in ending inventory without taking a physical count. The last-in, first-out (LIFO) method is one of the three inventory cost flow assumptions, alongside the FIFO (first-in, first-out) and average cost methods.

What Are the Disadvantages of a Periodic Inventory System?

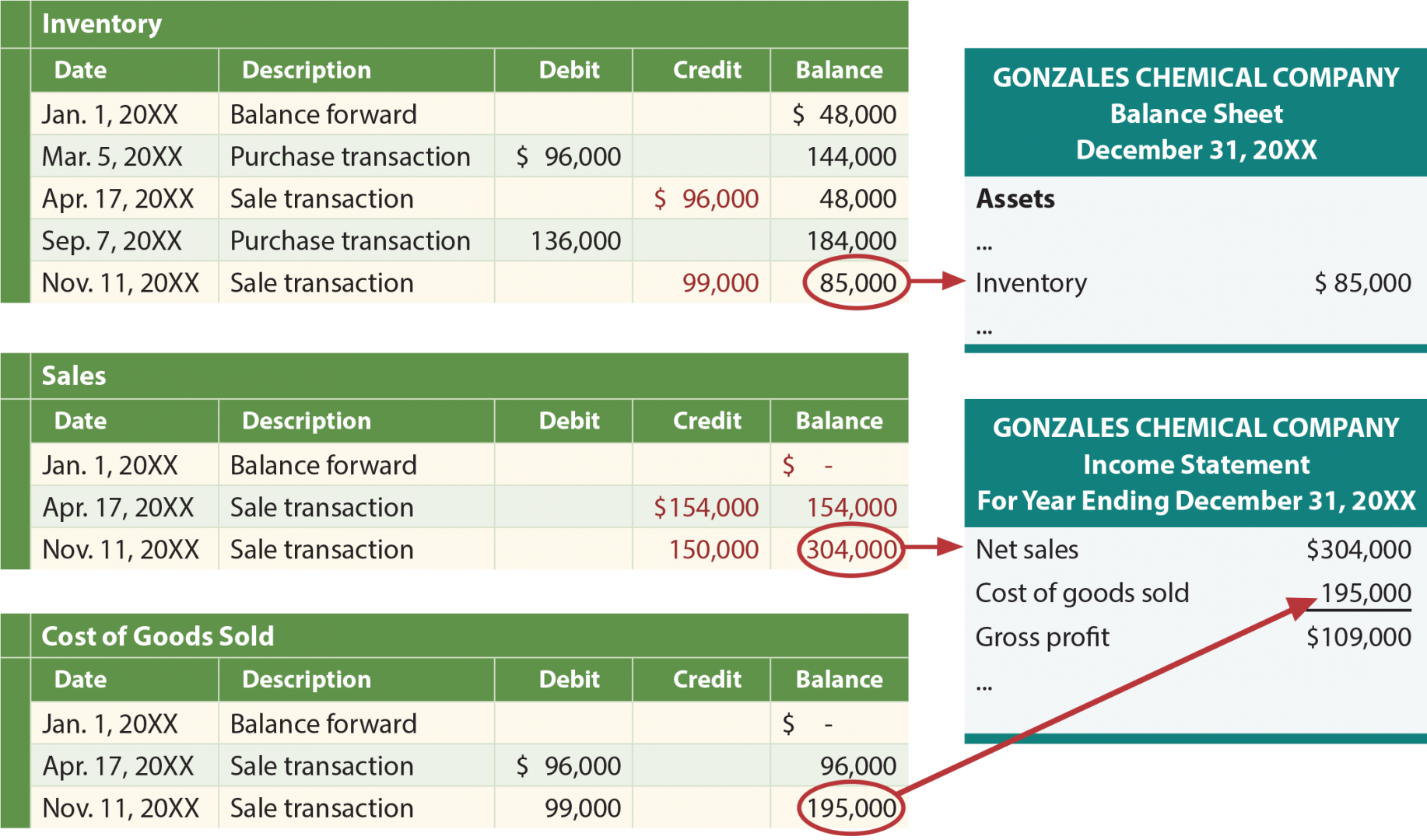

According to a physical count, 1,300 units were found in inventory on December 31, 2016. The company uses a periodic inventory system to account for sales and purchases of inventory. The goal of using the WAC is to give every inventory item a standard average price when you make a sale or purchase.

- We’re going to see that the average changes after each purchase in this case.

- Assume our physical inventory count reveals 80 units in ending inventory.

- Embracing LIFO can lead to significant tax advantages, especially in periods of rising prices.

- For example, SAP and Oracle Cloud can provide real-time data analytics, ensuring that businesses have access to up-to-date information.

High-Value or Fast-Moving Items

As inventory is stated at price which is close to current market value, this should enhance the relevance of accounting information. LIFO is extensively used in periodic as well as perpetual inventory system. In this article, the use of LIFO method in periodic inventory system is explained with the help of examples. To understand the use of LIFO in a perpetual inventory system, read “last-in, first-out (LIFO) method in a perpetual inventory system” article.

How to use LIFO for costs of goods sold calculation

For example, if you sold 15 units, you would multiply that amount by the cost of your oldest inventory. However, if you only had 10 units of your oldest inventory in stock, you would multiply 10 units sold by the oldest inventory price, and the remaining 5 units by the price of the next oldest inventory. Using the FIFO inventory method, this would give you your Cost of Goods Sold for those 15 units.

Periodic systems are more suitable for businesses not affected by slow inventory updates. These include emerging businesses, ones that offer services or companies that have low sales volume and easy-to-track inventory. Companies whose staff struggle with a perpetual system, for instance those with seasonal help, would also benefit from maintaining a periodic system. As their business grows, they can always institute perpetual inventory. The last-in, first-out method is an inventory cost flow assumption allowed in by US GAAP and income tax laws. The LIFO method proponents argue that the LIFO method improves the matching of revenues and replacement costs.

What is Periodic LIFO?

Such a situation will reduce the profits on which the company pays taxes. Notice how the cost of goods sold could increase if the last prices of the items the company bought also increase. What happens during inflationary times, and by rising COGS, it would reduce not only the operating profits but also the tax payment. A perpetual inventory system can utilize the FIFO (First-In, First-Out) or LIFO (Last-In, First-Out) method. The selection of FIFO or LIFO will depend on the particular needs and desires of the company. FIFO is more commonly used as it reflects a natural flow of goods in most industries where older items are sold before newer ones.

So the inventory left at the end of the period is the most recently purchased or produced. In a periodic system, companies calculate Cost of Goods Sold (COGS) directly after a physical inventory, as they do not keep it on a rolling basis, nor do they update it continuously after each transaction. They do not keep an inventory account in a periodic system since they debit all purchases to a purchase account. Once the period is complete, the company adds the purchase account totals to the inventory’s beginning balance.

Thus, after two sales, there remained 30 units of beginning inventory that had cost the company $21 each, plus 45 units of the goods purchased for $27 each. Ending inventory was made up of 30 units at $21 each, 45 units at $27 each, and 210 units at $33 each, for a total LIFO perpetual ending inventory value of $8,775. The specific identification method of cost allocation directly tracks each of the units purchased and costs them out as they are sold. In this demonstration, assume that some sales were made by specifically tracked goods that are part of a lot, as previously stated for this method. For The Spy Who Loves You, the first sale of 120 units is assumed to be the units from the beginning inventory, which had cost $21 per unit, bringing the total cost of these units to $2,520.

A growing company with an increasingly complex supply chain can benefit from adopting a perpetual inventory system. The real-time inventory data provided by this method facilitates better decision-making when it comes to purchasing, production planning, irs moving expense deductions and overall supply chain management. By leveraging modern technology such as barcode scanners and inventory management software, companies can efficiently monitor product movement throughout the supply chain, from procurement to sales.